Soffo helps plaintiff-side law firms decide which denied or underpaid home insurance claims are worth

attorney time before weak files become uneconomical and viable claims get missed.

Too small to analyze, too risky to skim

Average homeowners claim severity was about $20,062 in 2023.

Too small for deep review, too risky for shallow screening.

Bad intake decisions kill case economics

In Florida, average handling costs were $9,934 for litigated claims versus

$1,576 for non-litigated, so weak cases quickly erode profitability.

Catastrophe losses are raising claims

U.S. severe convective storm insured losses exceeded $50B in 2023, driving

more disputed property claims and raising the stakes of intake decisions.

Turn denial documents into

decision-ready case data

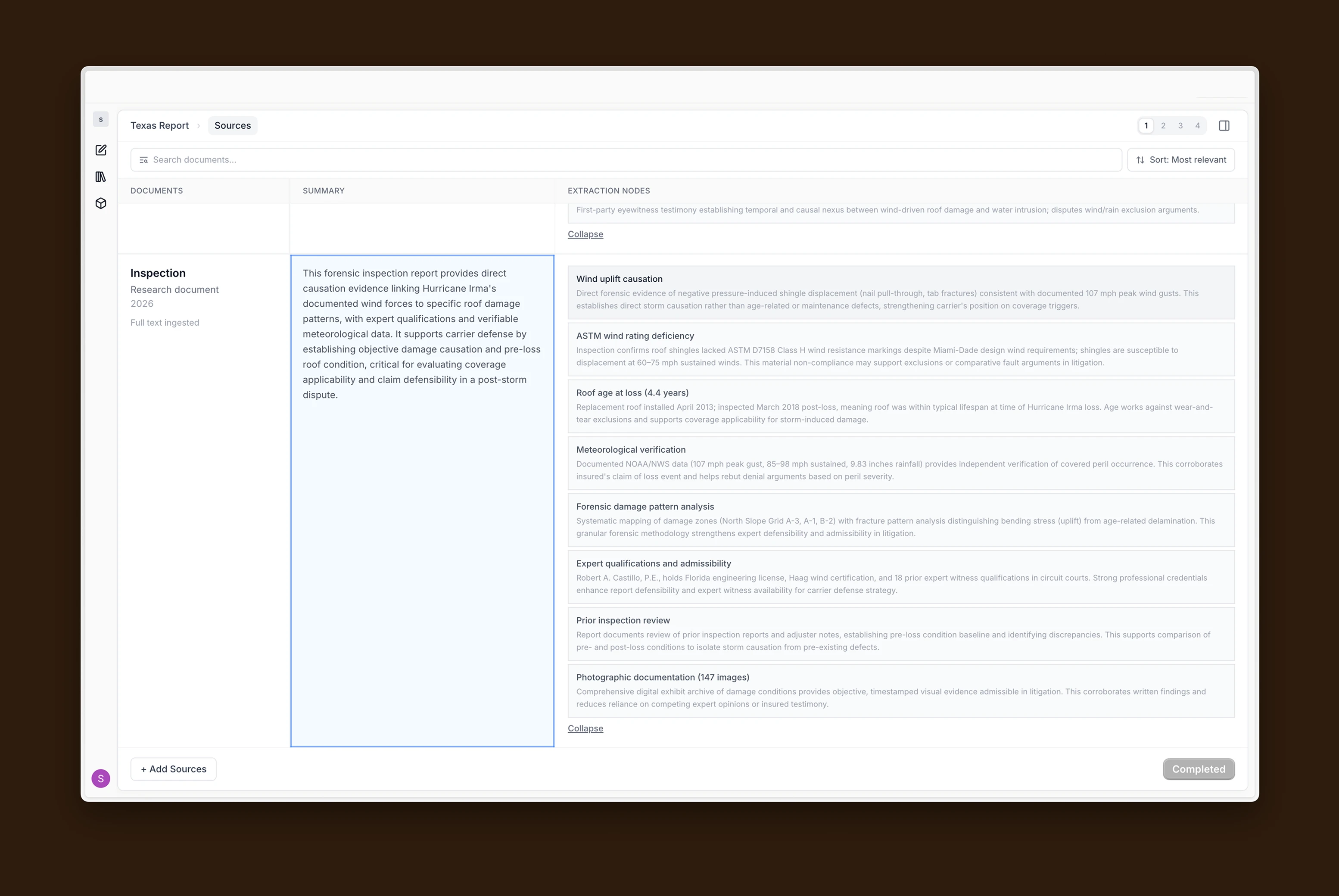

Soffo reads denial letters and converts them into

structured data mapped to its ontology, enabling fast,

consistent case evaluation without manual review.

Understand why a claim was

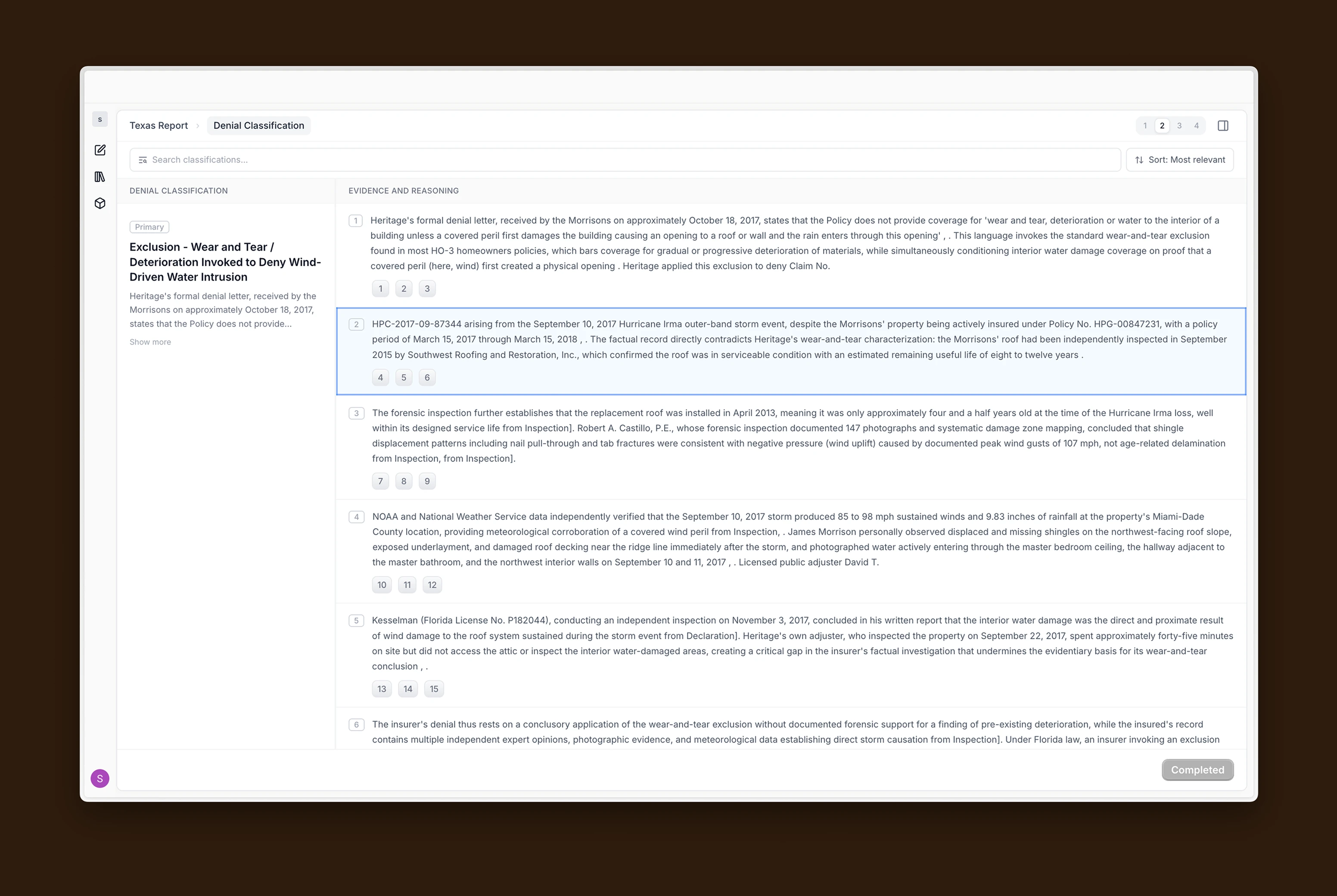

denied and whether to challenge it

Soffo identifies the exact reason for denial and

highlights which claims are legally attackable, helping

filter out weak cases early in intake decisions.

Estimate how strong the case is,

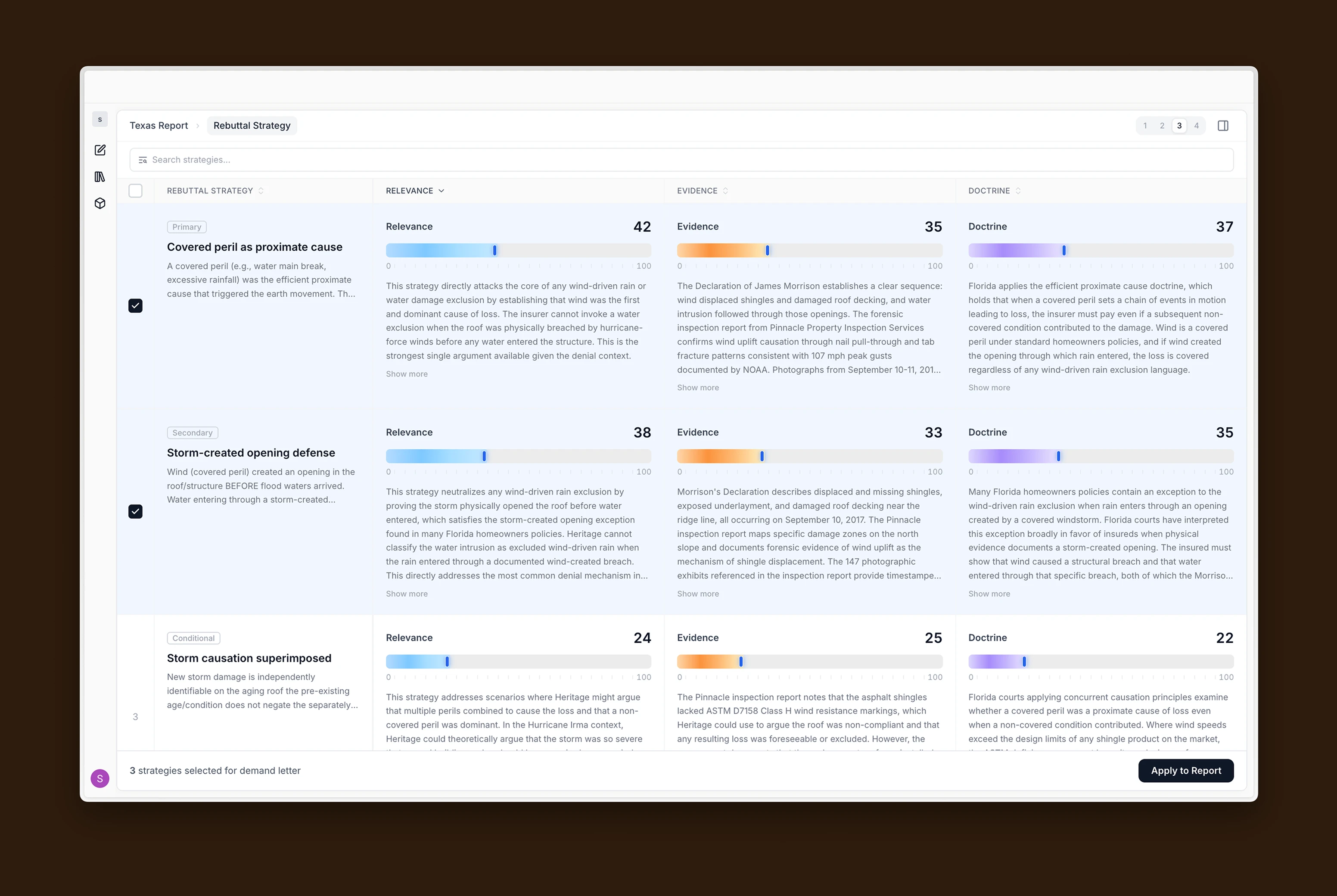

economically and strategically.

Soffo shows which rebuttal paths can actually work, what

evidence is missing, and what legal support exists behind them.

Show what a strong case

looks like in a concise report

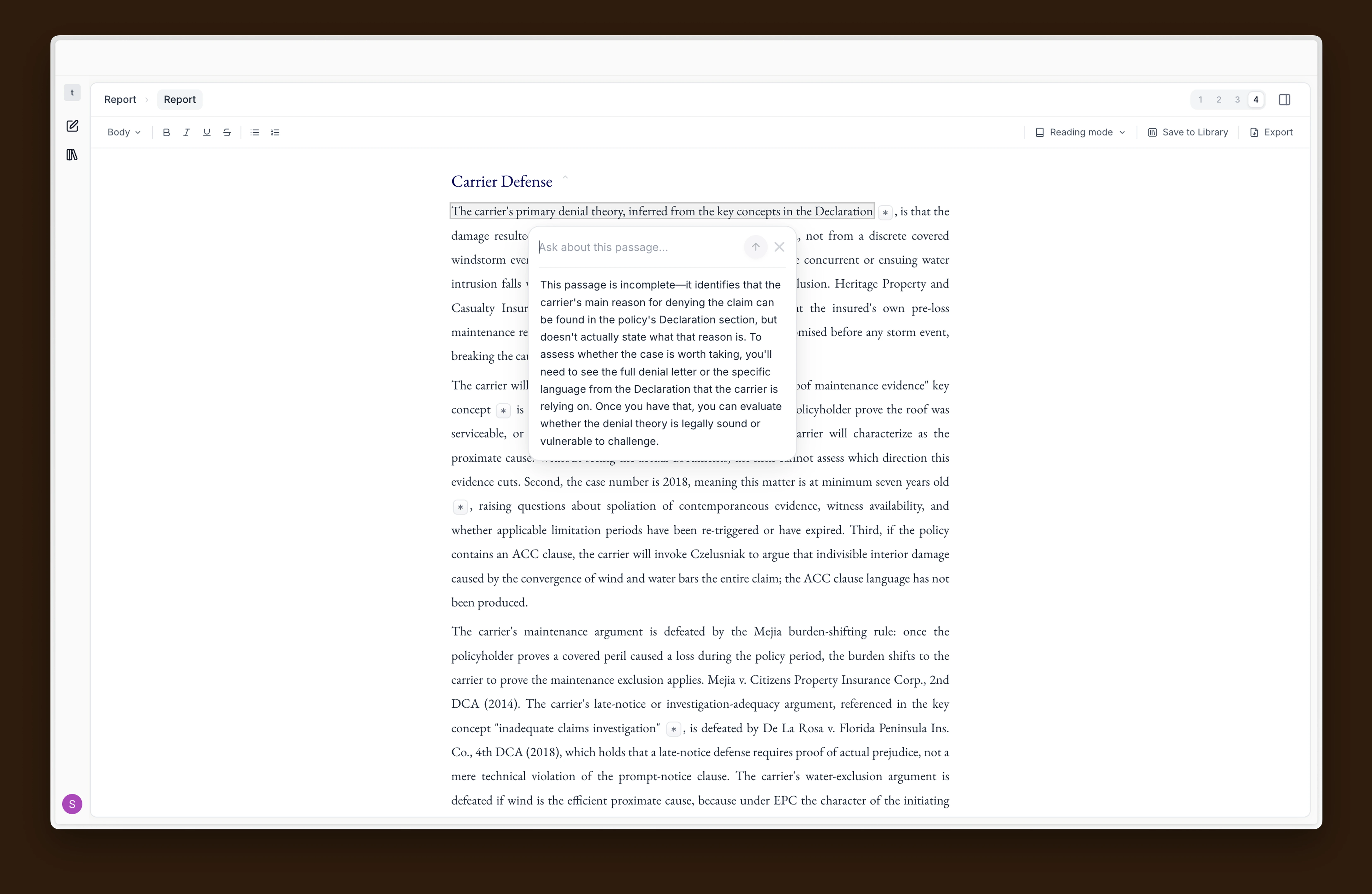

Soffo outlines the best way to argue the case upfront,

helping attorneys judge whether it is likely to settle or

stall before committing time and resources.

FAQs

Still have questions? Please contact

us at hello@getsoffo.com